We are halfway through 2026, and the new launch market has never had more moving parts. This mid-year overview gives you a grounded look at the key projects on sale today, the clusters quietly building across the island, and what the full picture means if a move is on your radar.

I was sitting with a young couple a few days ago. Let us call them Marcus and Jen. Both around late 30s, working in tech and marketing. They had just passed the five-year Minimum Occupation Period on their BTO, sold it for a decent profit of nearly $400,000, and were looking to upgrade. But they were nervous.

That conversation is what this article is essentially about. A walkthrough of everything happening in the new launch market right now: what is on sale, what is coming soon, what the government has in the pipeline, and what it means if you are thinking of making a move.

The surge in new launches in recent years is not random. It is the direct result of a busy run of Government Land Sales since towards the end of 2022, when the government released a higher volume of land to meet demand. Developers who won sites during those rounds have been coming to market at different stages ever since.

The key thing to understand is the time lag. From the moment a developer wins a GLS tender, it takes roughly one to two years before units go on sale, and another three to four years of construction before residents get their keys. The projects on sale today are essentially the result of land deals that happened about one to two years ago.

Which means the GLS sites being awarded right now in 2026 will likely only show up as new launches around 2027 to 2028. That gap between what you can see today and what is quietly building in the background is where most buyers get caught off guard.

The GLS programme has two tracks. The Confirmed List contains sites the government has committed to releasing regardless of demand. These will definitely come to market. The Reserve List contains sites that are identified and ready but will typically be triggered when a developer formally applies with an acceptable minimum bid, or when the government assesses sufficient market interest.

Reserve sites act as a pressure valve. If developers are hungry for land, they trigger reserve sites. If the market cools, those sites sit quietly on the shelf.

Both lists matter enormously for buyers. What sits on the reserve list adjacent to your shortlisted project is future supply that could compete with your unit at resale without you even realising it today.

With that framework in mind, let us look at what is actually sitting on the market right now.

As of early May 2026, buyers have a wide spread of choice across all three market segments: the Core Central Region (CCR), the Rest of Central Region (RCR), and the Outside Central Region (OCR). Here is what is actually on the ground.

The CCR covers Singapore’s most prestigious zones: Orchard, River Valley, Marina Bay, Bukit Timah, and their surrounding ultra-prime districts. Prices here generally sit above $2,800 psf, with flagship projects pushing far higher.

Current offerings include River Green (D9, 524 units, ~$3,1xx psf), River Modern (D9, 455 units, ~$3,2xx psf), and the ultra-luxury Skywaters Residences (D1, 190 units, ~$5,8xx psf). At the more accessible end of the CCR, Aurea at Beach Road (D1, 188 units, ~$2,8xx psf) offers a city-centre address with prices currently starting from around $2,6xx psf and entry-level quantum from approximately $1.7xx mil, a more viable entry point for buyers who want the CCR postcode without stretching into the ultra-premium tier.

Moving out from the city centre, the next tier down offers a different proposition entirely.

The RCR covers areas like Katong and East Coast (D15), Alexandra and HarbourFront (D3/4), and Paya Lebar (D14). It offers city fringe convenience at prices broadly between $2,200 and $3,000 psf.

District 15 is particularly active. Grand Dunman (1,008 units, ~$2,5xx psf), The Continuum (816 freehold units, ~$2,8xx psf), Meyer Blue (226 freehold units, ~$3,2xx psf), and Arina East Residences (107 units, ~$2,8xx psf) are all competing for the same broad buyer pool. The Continuum’s freehold tenure stands out sharply in a market where GLS projects are 99-year leasehold. For buyers thinking about generational wealth, that distinction is where the true legacy is built.

Further south, Canninghill Piers (D6, 696 units, ~$2,9xx psf) at Clarke Quay and One Marina Gardens (D1, 937 units, ~$2,9xx psf) represent the upper tier of the RCR, blending city fringe pricing with sought-after waterfront or MRT-integrated living.

Further out still, you reach the suburbs: where the bulk of demand, and the bulk of supply, currently lives.

The OCR covers Singapore’s suburban heartland and carries the bulk of new supply. It is where the majority of HDB upgraders are focused. The western OCR cluster (D21, D22, D23, part of D5) is especially supply-heavy, with Elta (D5, 501 units, ~$2,5xx psf), SORA (D22, 440 units, ~$2,2xx psf), Narra Residences (D23, 540 units, ~$2,1xx psf) and The Myst (D23, 408 units, ~$2,0xx psf) all vying for broadly the same buyers.

In the north and north-east, the Lentor corridor has become the defining OCR story of this cycle, and we will get into that in detail shortly. In the east, Parktown Residence (D18, 1,193 units, ~$2,3xx psf) is the standout project right now, combining sheer scale and direct access to the upcoming Tampines North MRT on the Cross Island Line.

Many of these are already on sale today. But the bigger story for a forward-looking buyer is what comes next.

Beyond current launches, a significant wave of projects is in development where land has already been acquired. These launches are coming: the only variable is timing. This is where careful buyers may gain an advantage by understanding the competitive landscape before it materialises.

Lentor in District 26 has quietly become one of the most exciting new residential clusters in the OCR. Within roughly a kilometre of Lentor MRT, you already have Lentor Central Residences (477 units, ~$2,2xx psf), Lentor Hills Residences (598 units, ~$2,1xx psf), Lentoria (267 units, ~$2,2xx psf), Hillock Green (474 units, ~$2,2xx psf), the upcoming Lentor Gardens Residences (499 units), and the latest Lentor Central Plot 4 GLS site awarded in March 2026 to the GuocoLand, Intrepid and TID consortium, and that is not even the full list. All in, we are talking over 4,000 units anchored by the Thomson-East Coast Line, with a maturing estate taking shape around it.

The earliest movers, Lentor Modern and Lentor Hills Residences, launched in 2022 and 2023 respectively, registering strong take-up rates and setting the pricing benchmark when the area was still fresh. Later entrants have had to price more carefully to attract buyers.

Lentor’s structural case, with direct Thomson-East Coast Line access to Orchard and the CBD, gives it genuine long-term staying power. But this is a patient buyer’s play. Capital appreciation here is likely to be measured, and probably not dramatic.

While Lentor anchors the OCR north, a very different story is taking shape in the east.

The Bayshore Drive confirmed GLS site, launched for tender in March 2026, is one of the most exciting plots to hit the market in years. At 5.74 hectares, it can yield up to 1,280 homes and 22,500 square metres of shops and amenities. This is not your typical condo launch. Think waterfront living along East Coast Park, built from the ground up as a proper mixed-use precinct.

Here is what makes it stand out. The whole development will be integrated directly with Bedok South MRT Station and a bus interchange, so you step out of your home and you are already connected. Add retail at your doorstep, park access right outside, and sea views to wake up to, and you start to see why this is distinctively different from most of what the OCR has to offer.

To put the scale in perspective, Bayshore is part of the 1H 2026 GLS Confirmed List, which is releasing 4,575 units in total across Singapore. That is 50% more than the average Confirmed List supply over the past decade. The nearby New Upper Changi Road GLS site adds another 1,040 units to this eastern corridor. The government is planting a big flag here, and many are starting to take notice.

Head west, and you find another ambitious new town taking shape, though on a very different timeline.

Tengah Garden Residences (863 units, District 24) is expected to obtain its TOP around September 2031, which is about five years away. The project also saw an overwhelmingly strong response during its launch in April this year, with nearly all 863 units snapped up over the launch weekend. The eco-town vision is compelling on paper. But right now it is a construction site surrounded by other construction sites. The MRT line is not open. The community has not formed.

If you are buying Tengah, you are making a long-term bet on a town that has not proven itself. That said, Singapore’s planning track record is excellent, and Tengah will likely mature into a fine estate. But go in with realistic expectations on early appreciation. The payoff will take time.

Back in the central corridor, the upcoming pipeline has its own set of projects taking shape, and they come with very different economics.

In the RCR and CCR pipeline, several major projects are currently in preparation. These include Dorset Road (UOL / Singapore Land, land cost $1,338 psf ppr) with an estimated yield of 428 units, Kallang Close (Frasers and Mitsubishi, land cost $1,415 psf ppr) projected at 470 units, and Dunearn House, which is slated to launch soon (CSC Land / Sekisui / Frasers), with an estimated yield of 380 units and a breakeven hovering around $2,558 psf.

On the luxury end, Delfi Orchard (CDL) has a breakeven approaching $4,995 psf, a flagship CCR luxury product aimed squarely at the ultra-premium segment. Buyers eyeing these projects need to go in with their eyes wide open on the math: high land costs are usually passed on in full, leaving developers with almost no wiggle room on their launch prices.

Most buyers look at what is currently on sale and stop there. The smarter move is to look at the full pipeline: GLS sites that have not yet been tendered or built, but which will eventually compete with any property you buy today.

Back to the tap analogy: the existing launches are the water already in your bucket. The upcoming confirmed GLS sites are the water about to flow in. The reserve sites are the extra tanks in the background, ready to open if the market calls for it.

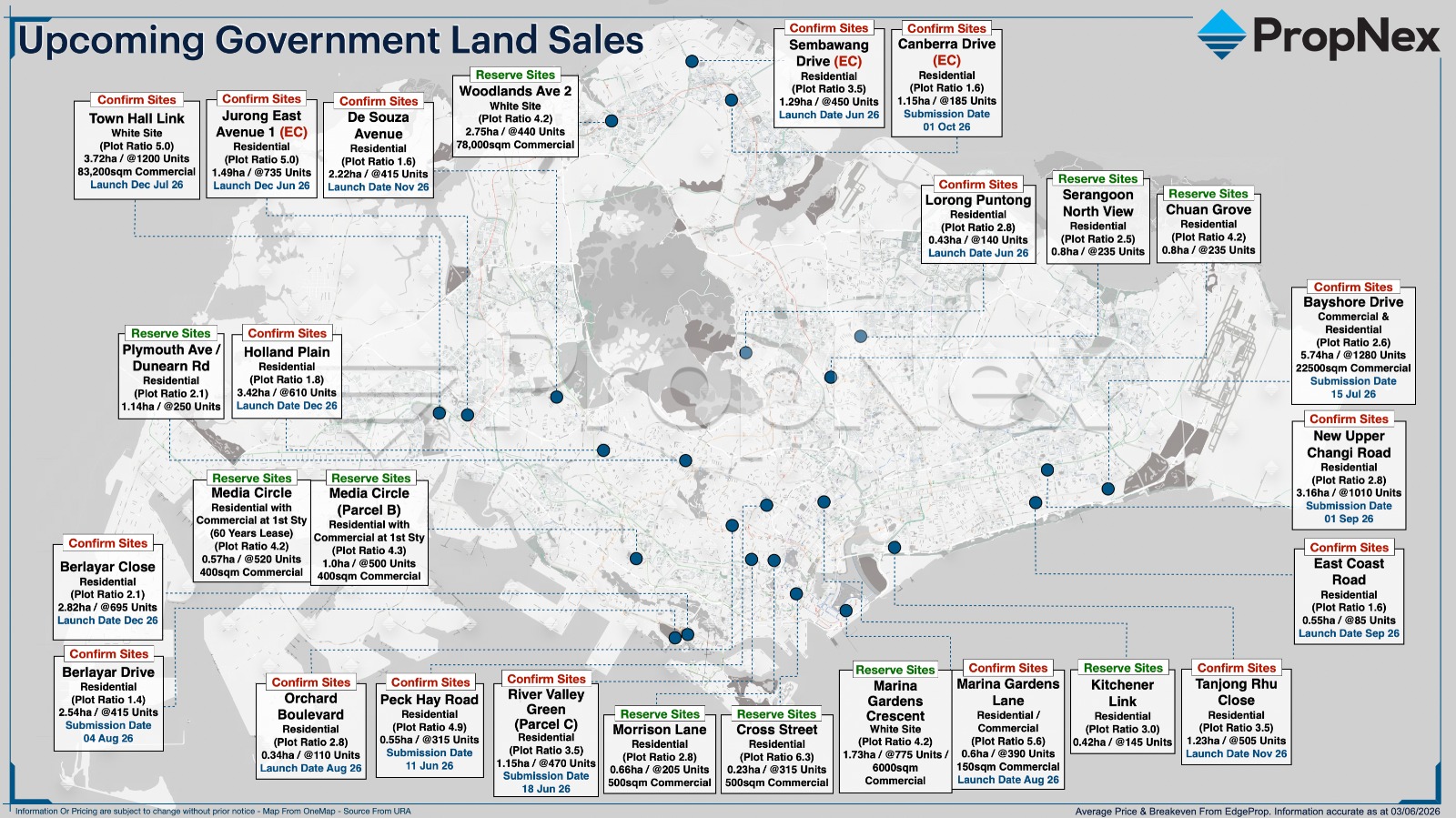

The government has committed to releasing these sites, and the numbers tell a compelling story. The 2H 2026 GLS programme, released on 3 June 2026, introduced nine new Confirmed List sites capable of yielding a combined 4,745 units, including 735 EC units. That represents a 3.7% increase from the 4,575 units offered in the first half, making it the highest half-yearly residential supply since 1H 2025. Add both halves together and the full-year 2026 Confirmed List stands at 9,320 units, more than 50% above the ten-year annual average. The tap, as we said earlier, is running wide open.

This pushes the total private housing pipeline (including Executive Condominiums) to around 61,000 units, up from roughly 57,000 previously. That figure is not a crash waiting to happen. Think of it more as a deliberate ceiling the government is building to keep prices from running away. And if you look at where the new sites are being placed, four of the nine 2H 2026 sites are concentrated in the city fringe (RCR). This tactical positioning is not accidental. The government is specifically trying to inject healthy supply choices into the active mid-tier segments before they face runaway pressure.

Fig. 3 — Upcoming Government Land Sales: Confirmed and Reserve Sites (PropNex Research, June 2026)

These sites will come to market in staggered waves. Here is what each one means for buyers:

| Site | Region | Est. Units | Key Notes |

|---|---|---|---|

| Marina Gardens Lane | CCR | ~390 | Shifted from Reserve List; near Marina South MRT; Gardens by the Bay views |

| Orchard Boulevard | CCR | ~110 | Boutique site off Orchard Road; extreme CCR land scarcity expected to drive keen bidding |

| Tanjong Rhu Close | RCR | ~505 | Adjacent to record-setting Tanjong Rhu Road plot; sea views on higher floors |

| De Souza Avenue | RCR | ~415 | Adjacent to The Sen; near Beauty World MRT; value play on Bukit Timah fringe |

| Berlayar Close | RCR | ~695 | Third GSW site; potential Keppel Bay & Mount Faber views; near Telok Blangah MRT |

| Holland Plain | CCR | ~610 | Third and largest Holland Plain site; near Methodist Girls’ School and King Albert Park |

| East Coast Road | OCR | ~85 | Boutique, low-rise Siglap enclave; 100sqm min. avg. unit size; niche developer play |

| Jurong East Ave 1 EC | EC / OCR | ~735 | First EC in Jurong East in ~30 years; near Toh Guan MRT (JRL); new 10-year MOP rules apply |

| Town Hall Link | OCR | ~1,200 + commercial | White Site; Jurong Lake District; 40,000 sqm office; tender July 2026; 4 MRT lines |

In aggregate, these confirmed sites represent several thousand additional units entering the market in staggered waves from 2027 to 2028 onwards. If any of these sits in the same micro-market as your shortlisted project, it is direct future competition for your resale buyers.

Reserve sites are identified and ready but only released when a developer applies and commits to a minimum bid. They can appear quickly and with limited public notice, which is precisely why buyers need to know they exist.

| Site Location | Segment | Area (ha) | Est. Units | Key Highlights |

|---|---|---|---|---|

| Serangoon North View | OCR / D19 | 0.80 | ~235 | Short walk to upcoming Serangoon North MRT on the Cross Island Line |

| Chuan Grove | OCR / D19 | 3.18 | ~935 | Third and largest plot in the Chuan Grove cluster; near Lorong Chuan MRT on the Circle Line |

| Plymouth Ave / Dunearn Rd | CCR / D10 | 1.14 | ~250 + 1,500 sqm commercial | Portion of former Raffles Town Club site; prestigious Dunearn Road address; near Stevens MRT |

With the full pipeline in view, let us now look at each region specifically. The picture looks very different depending on where you are standing.

The CCR and upper RCR landscape is characterised by a concentration of projects in a few key corridors: Robertson Quay and Great World (D3/9), Toa Payoh and Boon Keng (D12), and the Orchard-Buona Vista belt. Supply here is more measured than in the suburban zones, and that scarcity is not accidental. The government has been deliberate about keeping releases in these premium central corridors small and well-spaced, which provides a natural floor of support for values over the long run.

The upcoming and recently awarded central projects, including Kallang Close, Dunearn House at Turf City, and Dorset Road, will add fresh RCR and CCR supply over 2027 to 2028. The combined pipeline is large enough that buyers will have adequate choices, which keeps developers accountable on quality even if it moderates aggressive price growth.

The 2H 2026 Confirmed List adds further CCR and premium RCR supply to watch. Orchard Boulevard (110 units) is the most closely watched: limited new CCR land in this corridor, proximity to Orchard Boulevard MRT, and the strong take-up at nearby UpperHouse all point to keen developer competition at tender. Holland Plain’s third site (610 units) adds substantial luxury supply in that enclave, though its premium price quantum may temper broad buyer interest. Tanjong Rhu Close (505 units, RCR) sits adjacent to the record-setting Tanjong Rhu Road plot and could see similarly competitive bidding. Berlayar Close (695 units, RCR) adds to the Greater Southern Waterfront accumulation. Buyers looking at projects in any of these corridors should map the full three-site pipeline, not just the project immediately in front of them.

The western region is one of the most supply-dense zones in Singapore right now. In District 5 and its immediate central fringes alone, you have Elta, the record-setting Dover Drive GLS site, and multiple active plots coming to market at Media Circle. Further down in the Faber Walk enclave, Faber Residence adds even more low-rise volume to the west. That is approximately 2,200 units competing for a similar pool of buyers within a fairly compact area. Plenty of choice, but also plenty of competition.

Terra Hill (D5, ~$2,6xx psf) stands apart from the crowd for one simple reason: it is freehold. Freehold land along the Pasir Panjang hillside is rather scarce, and that scarcity tends to hold its value well over time. If you are buying with a long horizon in mind, that is a meaningful edge in a market where most of the surrounding options are 99-year leasehold.

Over in Jurong East (D22), J’Den, Sora, and The Lakegarden Residences all sit within close range of each other. The Jurong Lake District transformation is a real and exciting long-term story, but the key word there is long-term. We are talking 10 to 15 years before that vision fully plays out. Go in with realistic expectations on how quickly values will move.

Town Hall Link has been moved to the 2H 2026 Confirmed List, meaning it will definitely be tendered. The 1,200-unit mixed-use development, anchored by a minimum 40,000 sqm office footprint alongside retail and complementary lifestyle components, will be a defining addition to the Jurong Lake District. The tender launches in July 2026. For buyers already in or considering the JLD corridor, this confirms the long-term thesis but also signals significant additional residential supply coming in the next few years. On top of this, the Jurong East Avenue 1 EC site (735 units) adds the first EC in Jurong East in almost 30 years, which could absorb a significant slice of the HDB upgrader demand in that area.

The north doesn't tell one story. It tells two. The first revolves around the Lentor cluster in D26, which we've already unpacked. The second centres on a busy and growing pipeline stretching across Yishun, Sembawang, Canberra, and Woodlands, and there's plenty to dig into here.

Starting with private housing, Upper Thomson Road A brings 595 units to a corridor already well-served by the Thomson-East Coast Line. But the one to watch is the upcoming Chencharu Close mixed-use development, which will introduce 875 private units into the Yishun and Khatib area. That's a significant number for a neighbourhood long dominated by public housing, and how this launch performs will set a real benchmark for private residential activity in the area going forward.

The EC market up north is equally lively. Between Miltonia Close EC (430 units), two ECs at Woodlands Drive 17 (432 and 560 units respectively), and the Sembawang Road EC (265 units), there's a healthy spread of options for qualified buyers. With this much choice on the table, buyers in this corridor are in a strong negotiating position. That said, there's one important distinction worth flagging before anyone starts comparing projects side by side.

Not all of these sites operate under the same framework. The legacy sites mentioned above fall under the previous set of rules, which means they still carry the classic 5-year Minimum Occupation Period and offer the option of a Deferred Payment Scheme.

The newer GLS EC sites at Canberra Drive and Sembawang Drive, however, are a different matter entirely. These are the first sites to come under the government's new rules announced on 8 May 2026, which introduced a mandatory 10-year MOP and removed the Deferred Payment Scheme option altogether. It's a pivotal shift, and for buyers weighing up their options across this corridor, understanding which rules apply to which site isn't just useful background. It could be the deciding factor.

We will cover what this means for you shortly.

The east remains one of the most consistently in-demand residential zones: good schools, vibrant food and beverage culture, excellent connectivity, and an unmistakable community character. Parktown Residence (D18, 1,193 units, ~$2,3xx psf) is the headline project. Its massive scale creates its own integrated amenity ecosystem.

If you are seeking structural asset longevity, Kassia (D17, 276 freehold units, ~$2,1xx psf) offers rare, entry-level freehold land in the eastern suburbs. If lifestyle and pure convenience are the priorities, Pinery Residences (D18, 588 units, ~$2,5xx psf) injects premium leasehold supply directly linked underground to Tampines West MRT. Meanwhile, the mega en bloc redevelopment of Loyang Valley by SingHaiyi (1,249 units, ~$940 psf) in Loyang subzone is a major 99-year leasehold play to watch, perfectly positioned to capture the massive workforce catchment of the Changi Aviation Cluster.

The two confirmed GLS sites, Bayshore Drive and New Upper Changi Road, will define the next chapter of eastern development. Bayshore in particular is not just another OCR enclave, it is a waterfront precinct transformation with a compelling long-term thesis.

The 2H 2026 GLS adds one eastern site to the pipeline: East Coast Road in the OCR, bringing around 85 units to the Siglap landed enclave. As the smallest plot on the 2H Confirmed List, it won't move the needle on supply pressure in the east.

Connectivity is worth a mention. At roughly 800 metres from Siglap MRT, it's not a doorstep-to-station situation. But the immediate lifestyle offering at Siglap V and the surrounding café stretch goes a long way to compensating for that.

The site confirms continued government interest in activating land along the TEL corridor, though buyers seeking masterplan-scale supply will find the bigger story remains Bayshore and New Upper Changi Road.

All of this regional data points to a few patterns worth highlighting. These are the things that differentiate an informed buyer from one who simply buys what the agent shows them.

The clustering patterns visible in the regional maps are structural. When the GLS programme releases land in a given area across successive rounds, multiple developers each win a plot within a similar timeframe, develop on similar timelines, and launch within the same 18-month window.

For buyers, supply clustering has a couple of short-term benefits (wide product choice and competitive developer pricing) and a medium-term challenge (more intense resale and rental competition when those projects all reach TOP within a similar window). The projects that hold values best in a clustered zone are those with a distinct edge: direct MRT access, freehold tenure, a waterfront or park-facing aspect, or a strong developer brand.

Understanding the supply wave in your area of interest is step one. Step two is understanding what the developer actually paid for the land.

The 2H 2026 Confirmed List makes a point of clustering sites near recently awarded plots: Orchard Boulevard, De Souza Avenue, Tanjong Rhu Close, Berlayar Close, and Holland Plain are all adjacent or close to GLS sites sold in the past two years. Industry analysts note this serves a dual purpose: building critical mass in emerging precincts and reducing the scarcity premium developers might otherwise bid aggressively to capture. For buyers, this is a useful signal that the government is actively managing land-price inflation by ensuring a steady nearby supply.

The estimated breakeven price is the minimum psf at which a developer can recover land cost, construction, and overheads. It is one of the most underused buyer metrics, and one of the most useful.

In a weaker market, developers rarely sell below breakeven for sustained periods. This creates a natural price floor, which is reassuring for buyers in those projects. But high breakevens also mean almost no buffer for developer flexibility: you as the buyer absorb the full cost of expensive land. Take Dorset Road, a prime city-fringe RCR site awarded at $1,338 psf ppr, and compare it with Lorong Chuan, where the developer swept up Chuan Grove Plot 1 and Plot 2, both OCR sites, to combine them into a single mega-site, paying up to $1,376 psf ppr for the land.

A developer paying a higher land rate for a suburban site than a true city-fringe plot tells you everything about how compressed the traditional pricing gap has become, and how much the market's pricing logic has shifted.

Now, let us talk about ECs. The rules have just changed in a big way, and if you are even remotely considering one, you need to read this carefully.

Executive Condominiums remain one of the most financially smart options for eligible Singaporean families. Built to private condo standards, priced 15 to 25% below comparable private condos, and CPF grant-eligible. If your household earns below $16,000 per month, ECs deserve a serious look before you default to a private condo.

That said, three significant rule changes took effect on 8 May 2026:

For EC GLS sites where tender closes on or after 8 May 2026. Full privatisation also shifts to 15 years. Plan your holding horizon carefully before committing.

Buyers must now follow the normal progressive payment schedule during construction. Cash flow planning over the build period becomes more important than ever.

Allocation for first-timers increases from 70% to 90%, with the priority window extended from one month to two years. If you are a genuine first-timer, your ballot odds have improved meaningfully.

Importantly, these changes only apply to new EC GLS tenders from 8 May 2026 onwards. Projects already launched or tendered before that date remain under the original five-year MOP framework. For instance, the incoming Sembawang Drive, Canberra Drive, and newly announced Jurong East Avenue 1 GLS EC will all fall under the new framework.

The Jurong East Avenue 1 EC (735 units), newly announced under the 2H 2026 GLS Confirmed List, is the first EC to be offered in Jurong East in nearly 30 years. It will be subject to the new May 2026 rules. Given the long absence of EC supply in Jurong East and the proximity to Toh Guan MRT on the Jurong Region Line and the Jurong Lake District, analysts expect strong demand from both first-timers and HDB upgraders. For eligible buyers in the west, this is one to watch closely when it eventually comes to tender.

On overall EC supply: the full-year 2026 Confirmed List now sits at 1,370 EC units across three plots, substantially below the 1,970 EC units offered in 2025. This measured supply likely reflects a transitional phase as the government monitors how developers and buyers respond to the May 2026 rule changes before releasing more EC land.

For a full breakdown of the changes, including a project-by-project guide on which rules apply, you can read the detailed overview here: EC Policy Changes: May 2026 →

Outside of ECs, another question comes up constantly in buyer conversations. Does it still matter whether a project is freehold or leasehold?

The short answer is yes, but context determines how much. Freehold projects typically command a 10 to 20% premium over comparable 99-year leasehold projects in the same area. For buyers with a 20-plus-year horizon or those thinking about generational wealth transfer, freehold in a well-connected, supply-constrained location is a logical long-term store of value.

For buyers planning to sell within five to ten years, MRT access and location quality almost always matter more than tenure. A well-located leasehold project in a strong corridor could outperform a freehold project in a remote or poorly connected area.

With all of this in mind, what does it actually mean for you specifically if you are thinking of making a move? The answer depends on which stage of the property journey you are at.

If you bought your HDB before 2019, crossed your MOP, and are sitting on solid paper gains, the current market presents a decent window to move. Yes, HDB resale prices dipped 0.1% in Q1 2026, the first decline in nearly seven years, but values remain historically high, meaning your exit price is still strong. And with so many new launches to choose from, you are in a position of real strength as a buyer.

Here is how to approach your upgrade thoughtfully:

If you already own a private condo, the current landscape offers three broad paths.

Upgrading makes sense if your current project is in a supply-heavy corridor with limited differentiation, or if there is an opportunity to trade up to a better-located or freehold project in a stronger belt. The mathematics depend on your existing equity, your current loan position, and your income sustainability.

Rightsizing, which means moving to a smaller but higher-quality unit in a better location, is worth exploring if your household size has reduced or you are approaching retirement and want to unlock equity while reducing monthly outgoings. This strategy is underused and often financially very sensible.

Holding makes sense if your current project has strong fundamentals: good MRT access, low nearby supply, an established community, and a credible developer brand. Do not sell just because the market looks busy around you. Move when it makes financial and lifestyle sense for your specific situation.

One specific note: map the GLS confirmed and reserve sites within 500 metres of your current project. If a large site is sitting there, that future supply will compete with your unit when you eventually want to exit. It tells you exactly when to cash out before the market gets crowded.

Supply is abundant. There are more choices across more price points and more locations than at any point in recent memory. That is good news for buyers who have been sitting on the fence. You are no longer chasing a scarce market.

But not all supply is equal. The clusters, including Lentor, the Jurong belt, and the EC-heavy north, have so much concentrated supply that buyers need to choose carefully. First movers in a new cluster have historically fared better than late entrants. Buyers who walk into a supply-dense zone without understanding the competitive landscape can find themselves holding a unit in a very crowded resale market five years later.

The GLS pipeline makes one thing clear: supply is not letting up anytime soon. New sites are being released across all three regions, which should keep a lid on runaway price growth in the OCR. That said, well-loved residential areas like Bayshore, Holland Plain, Upper Thomson, and established RCR pockets like District 15 are a different story. They continue to retain strong structural price support due to strict land-use zoning and physical limitations that constrain long-term private supply.

ECs remain the most financially efficient option for eligible buyers and deserve serious consideration. The rule changes of May 2026 mean you now need to be clear on which projects fall under the old framework and which fall under the new one before committing. In the CCR, quality projects in constrained corridors will always find buyers, but it is not a zone for those without adequate financial depth and long holding horizons.

In property, timing and location are not competing priorities. They are complementary ones. The best outcome comes when you align both: a location that fits your life and your budget, entered at a point when your financial position is ready. That intersection is different for every buyer, and finding it is the whole point.

Use this supply map as your compass. Understand what is in front of you, what is coming behind it, and what the government has planned further down the road. Then make a decision grounded in evidence, not in FOMO, not on impulse, and not in the last launch ad you saw on your commute.

If this article has raised more questions than it has answered, that is exactly the right response. Every buyer’s situation is different. The right project for Marcus and Jen may be entirely wrong for someone in a different financial position, at a different life stage, with different goals.

A proper advisory conversation does not begin with listings. It begins with your numbers, your goals, and a close read of what the supply map looks like for the areas on your shortlist. From there, we work through the options together: methodically helping you make a decision you will still feel confident about five years from now.

Whether you are an HDB upgrader taking your first step into the private market, an existing condo owner weighing your next move, or simply someone who wants to understand what is actually happening before making any decision at all, the right starting point is always the same: a simple and open conversation.

Reach out when you are ready. We will take it from there.

Not sure which project fits your situation? We can walk through your budget, your timeline, and the supply map for the areas on your shortlist, so you leave the conversation with a clearer picture than when you came in.

💬 Talk It Through →

All psf figures cited for launched projects reflect average transacted prices as at May 2026, sourced from URA. For upcoming projects, psf figures reflect estimated breakeven prices sourced from EdgeProp. Project data, land costs, and unit counts are drawn from PropNex Research (May 2026), URA, and EdgeProp. EC policy changes are referenced from HDB announcements dated 8 May 2026. Map data from OneMap. All figures are subject to change without notice and should be verified directly with HDB or URA before any property decision is made. This article is for general informational purposes only and does not constitute financial or investment advice.