Singapore Property Calculators User Guide

新加坡房地产计算机指南

Welcome!欢迎!

Thank you for using our Property Financial Calculators app.

These tools are commonly used by property agents for their real estate work and now, you can use it to do some self-assessment. Great, isn't it?

We will be gradually coming out with more user guides to help you discover the full potential of the calculators, so stay tuned.

In the meantime, do get in touch with us if you have questions!

感谢您使用我们的新加坡房产投资计算机App。

这些计算机是房地产经纪常用的工具,您现在也可以使用它进行一些自我评估!👍

我们将逐步推出更多的用户指南,以让您更有效的使用,敬请期待。

如果您有任何疑问,欢迎随时与我们联系!

This calculator work out the funds required for the purchase of executive condominium under the Deferred Payment Scheme.

Under this scheme, buyer just need to pay for the 20% downpayment and stamp duty fee and deferred the balance 80% till nearer to move in date. This will allow buyer time to buid up their funds like sale of their current HDB flat.

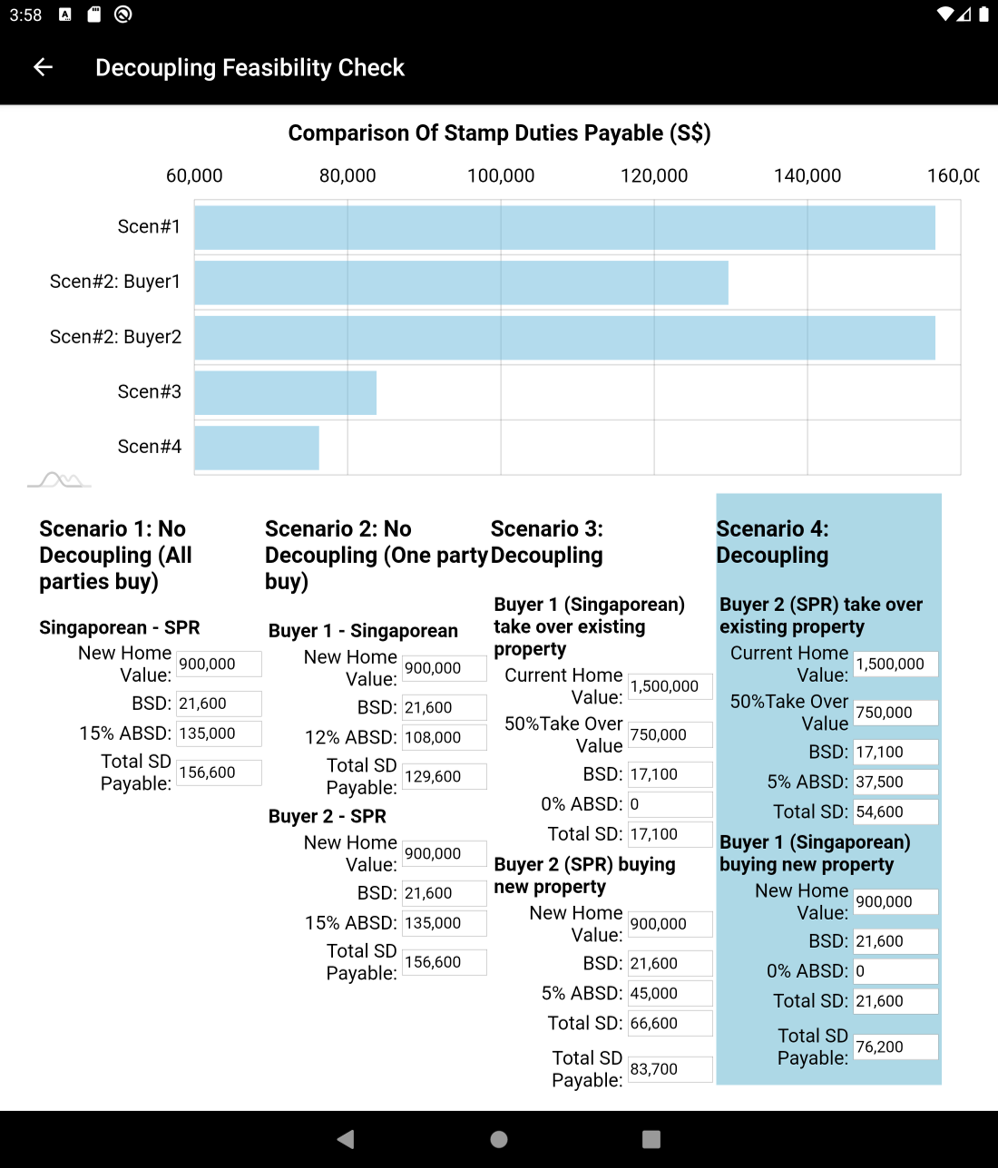

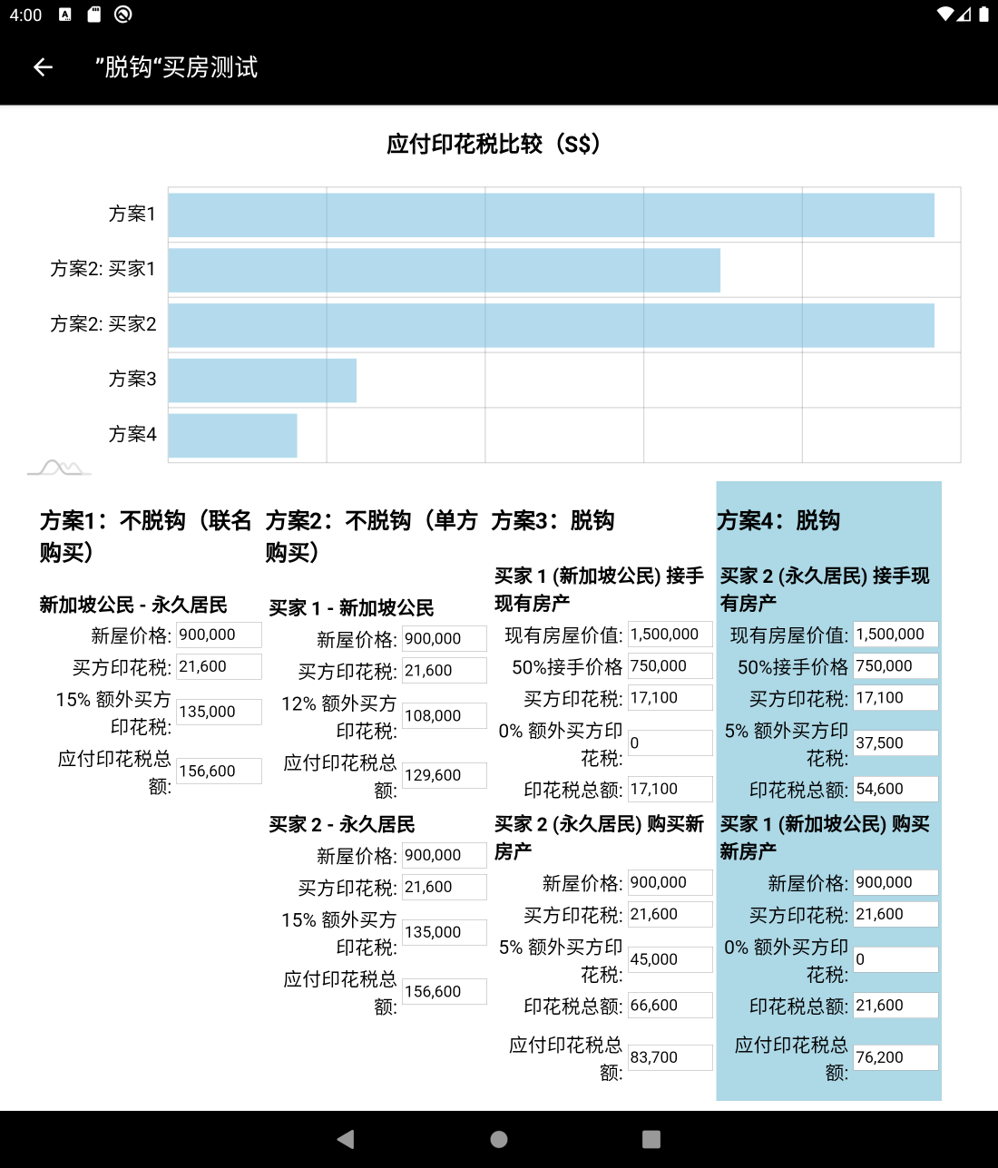

Most of the time when buying the next property, the no. 1 consideration is Additional Buyer's Stamp Duty - ABSD. This app allow you to work out the best way to restructure your portfolio for the holding of the next property.

By going through the Decoupling Feasibility Check, you can compare how much stamp duties payable for each option and decide which cause of action to take?

Please take note that this app did not take into the consideration of legal fee involve and the CPF top-up required for the part selling.

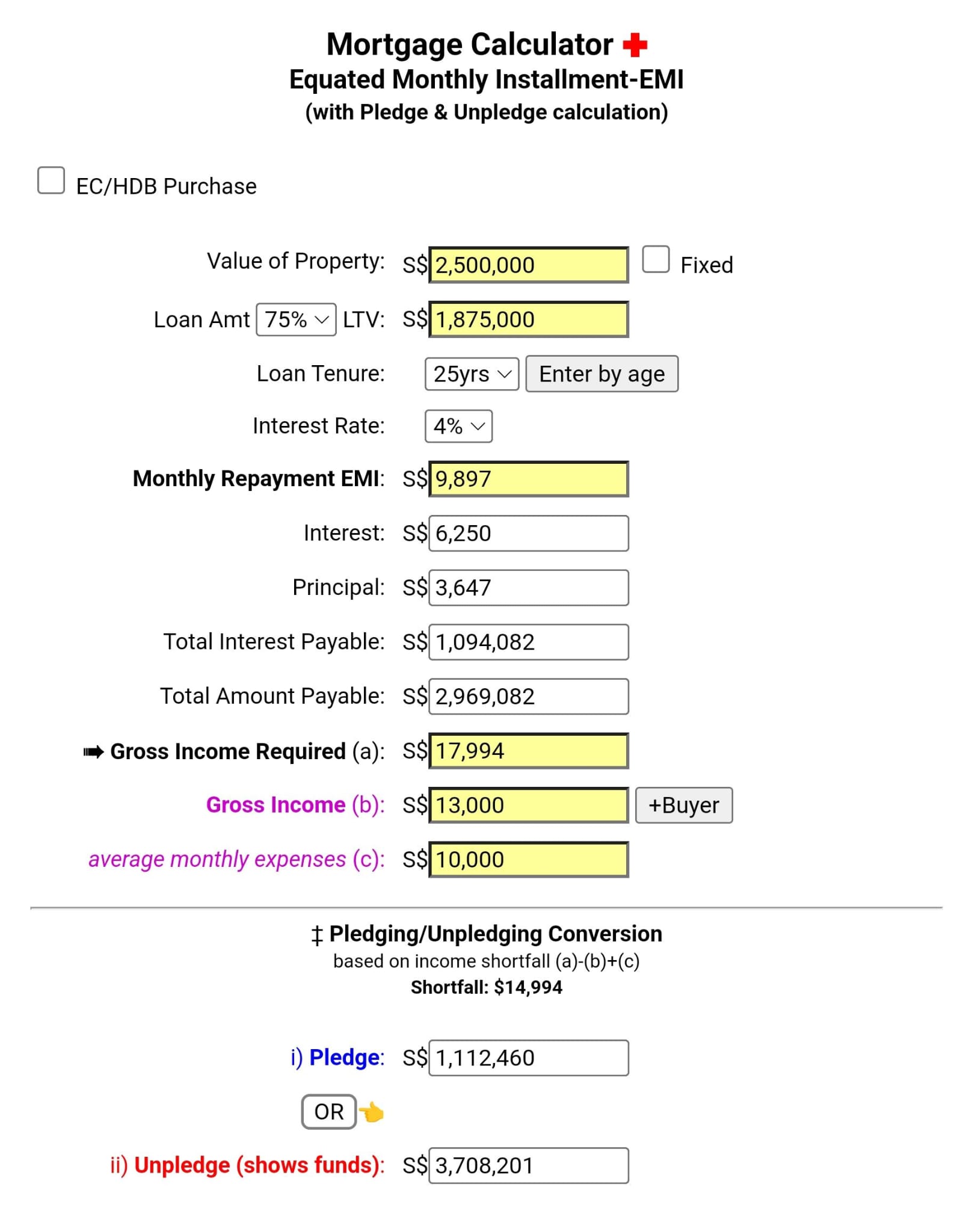

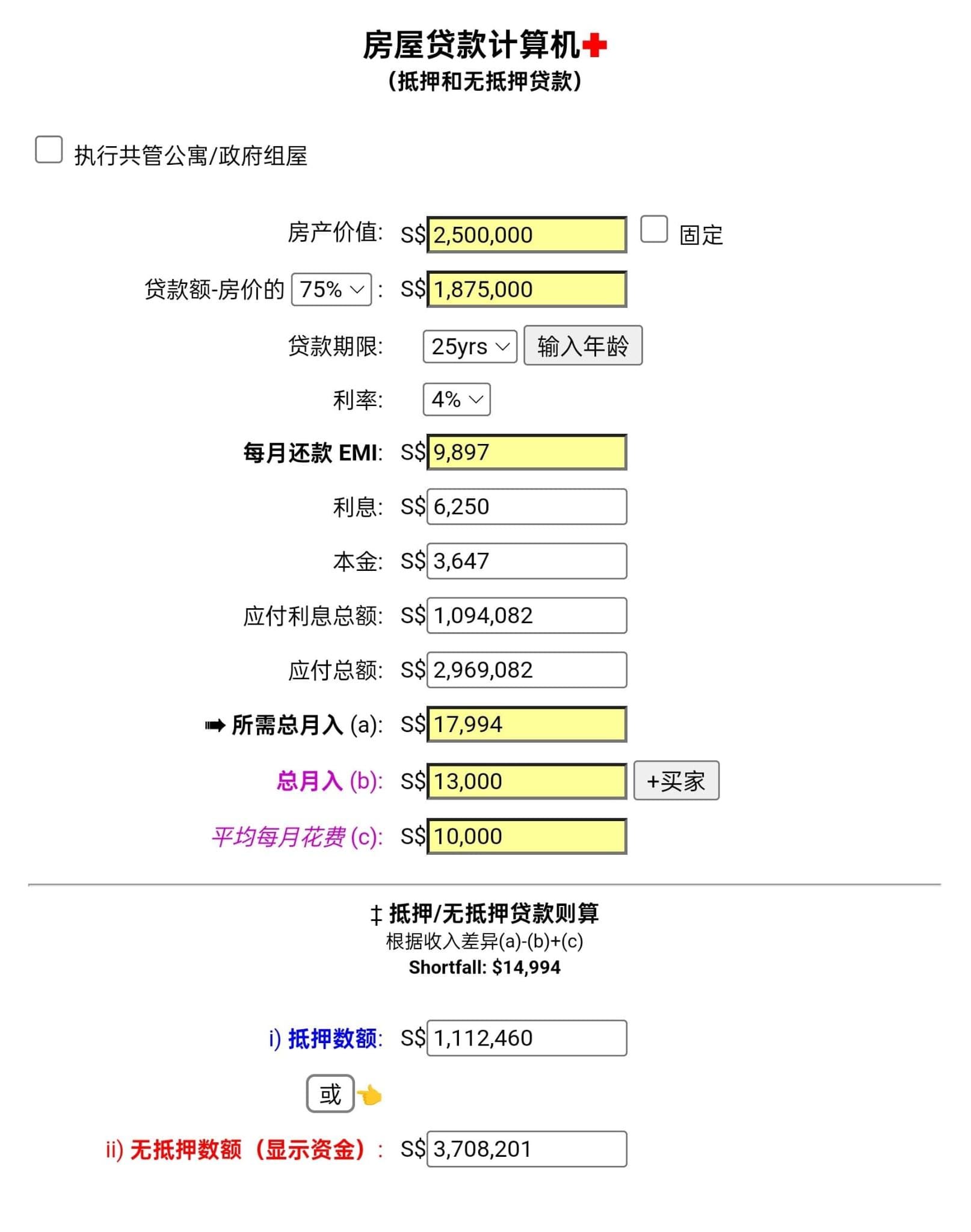

This calculator will give you a quick estimation of the amount of income you would need to qualify for a 75%(example) mortgage loan versus the actual income you have.

In the event of a shortfall, you may use Pledging or Unpledging of Asset(s) to top up the shortfall.

These features are useful if you have a pool of funds that you could tap on without actually spending it!

Pledging of Assets

Placement of cash as a fixed deposit with a legit financial institution for a period of 48 months or four years as a form of additional Monthly Gross Income. This is to calculate the final loan amount:-

Monthly Gross Income Derived = Pledged_Amount/48

Scenario:

Parents may have the funds and wish to support their child by making up for the shortfall. This amount can be deposited in the child's bank account as a fixed deposit for four years.

Unpledging

Showing of assets twice to the financial institution. Usually it's once during signing of contract, and before the first disbursement of funds to the developer.

Assets can be in the form of Cash, Gold, Stocks, Foreign Currencies, etc. Apart from cash, the value of the other assets will be determined by the financial institution that is offering the mortgage loan.

The formula to derive the equivalent monthly income is:-

Monthly Gross Income Derived = (Pledged_Amount/48)x30%

For instance, cash flow meant for business expansion could be used to show funds. In this way, the funds will not be locked up with the bank as a fixed deposit.

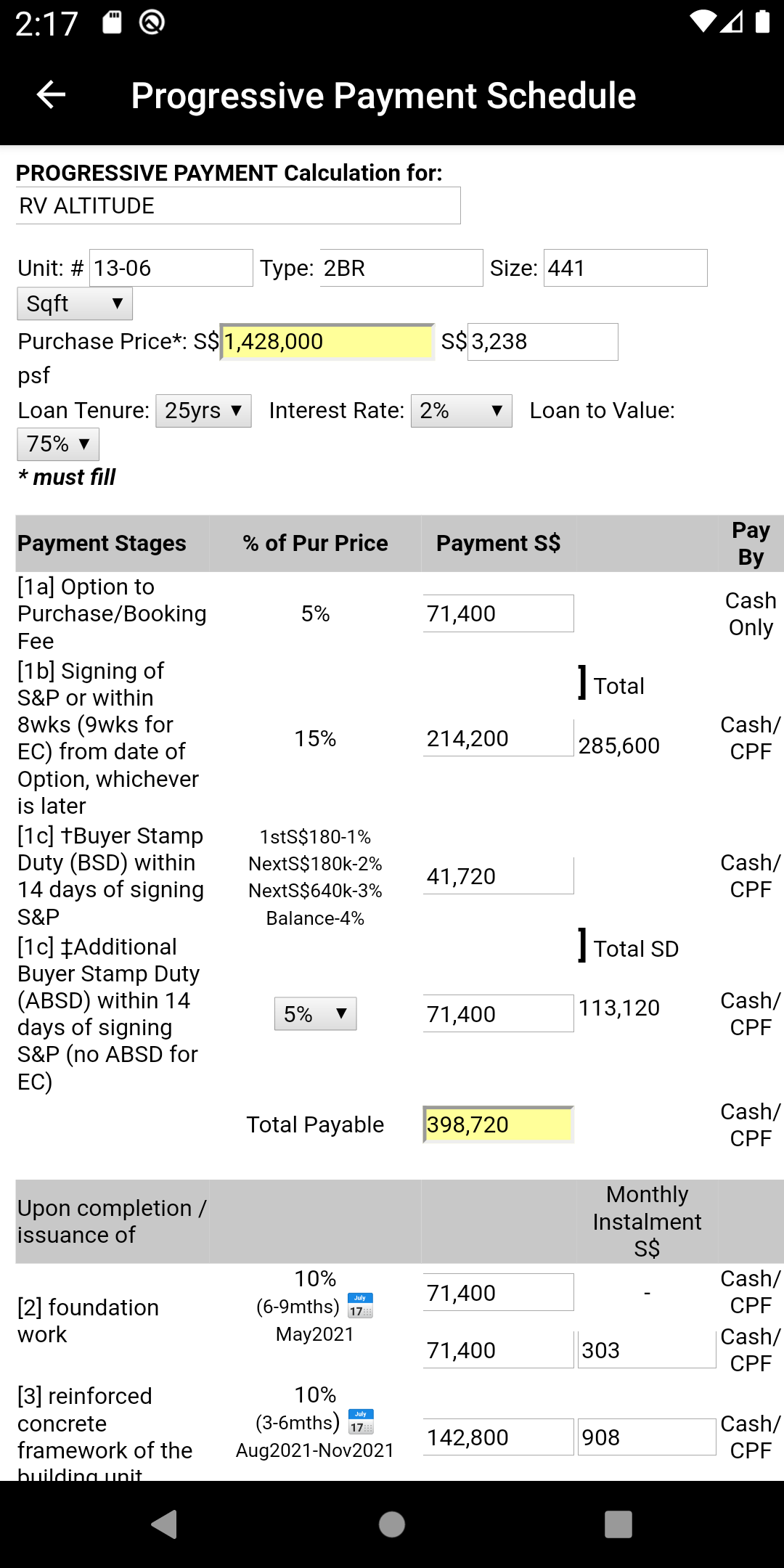

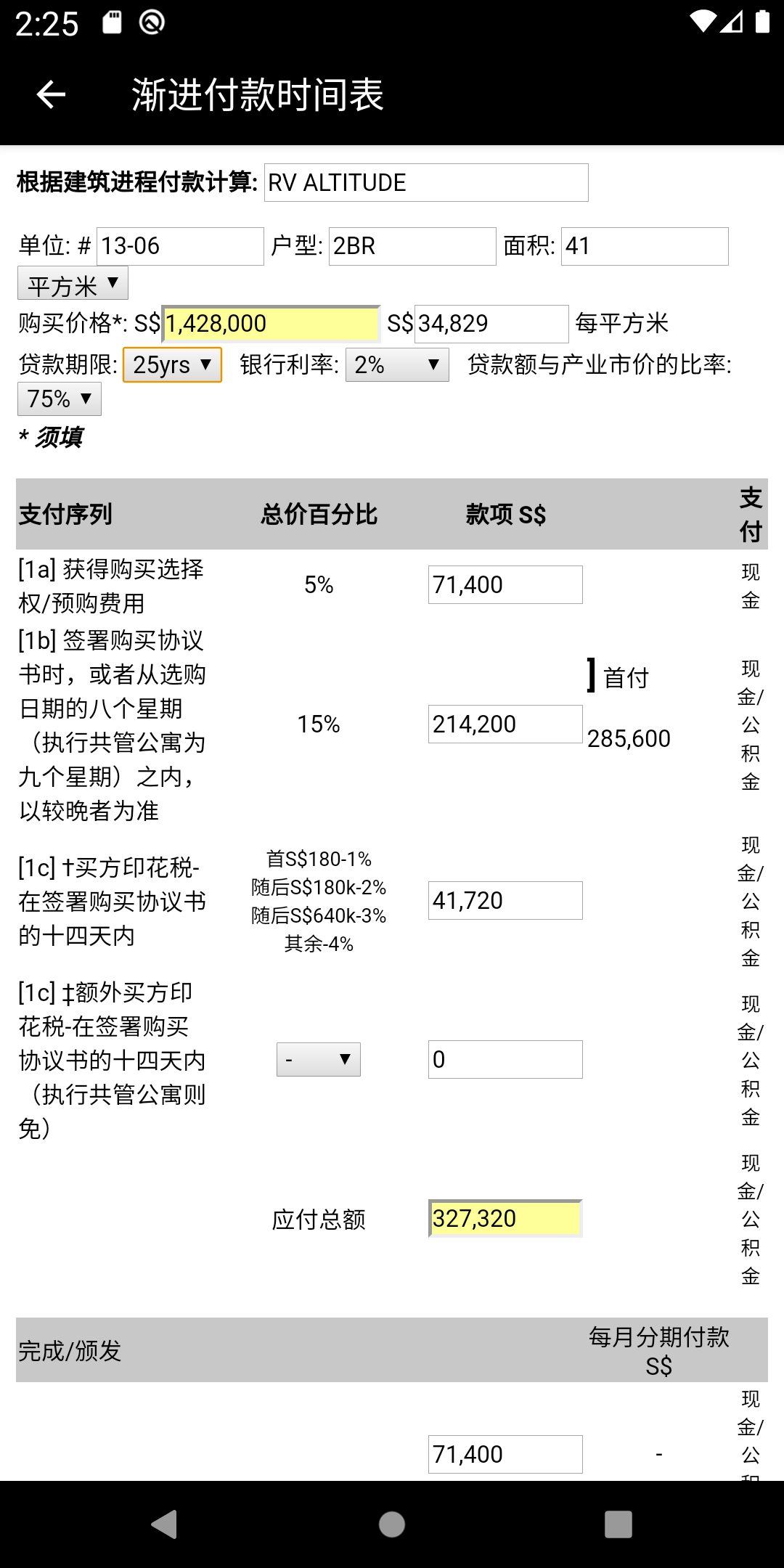

For new launches, the Progressive Payment Schedule🗓️ allows a buyer to plan for the funds requirement at the different stages.

A buyer can also use this calculator to work out the maximum value of a property he can buy with his available funds💵 for the down payment.

In other words, this progressive payment calculator can assist you to work out the fund requirements you need at the various stages based on the value of the property you wish to acquire or the value of the property price based on the budget you have for the initial down payment. However, basic knowledge of regulations relating to bank loans and ABSD (additional buyer's stamp duty) will be required to select the relevant input.

Users are advised to seek professional advice prior to purchase.

What makes many buyers hesitate to buy their next property?

If I say it's the Additional Buyer's Stamp Duty (ABSD), I think the reality could not be further from the truth! Like it or not, ABSD is here to stay, and it's likely to go higher over time.

So, it's time to start working out your next property purchase using our 🏠Property Investment Calculators.

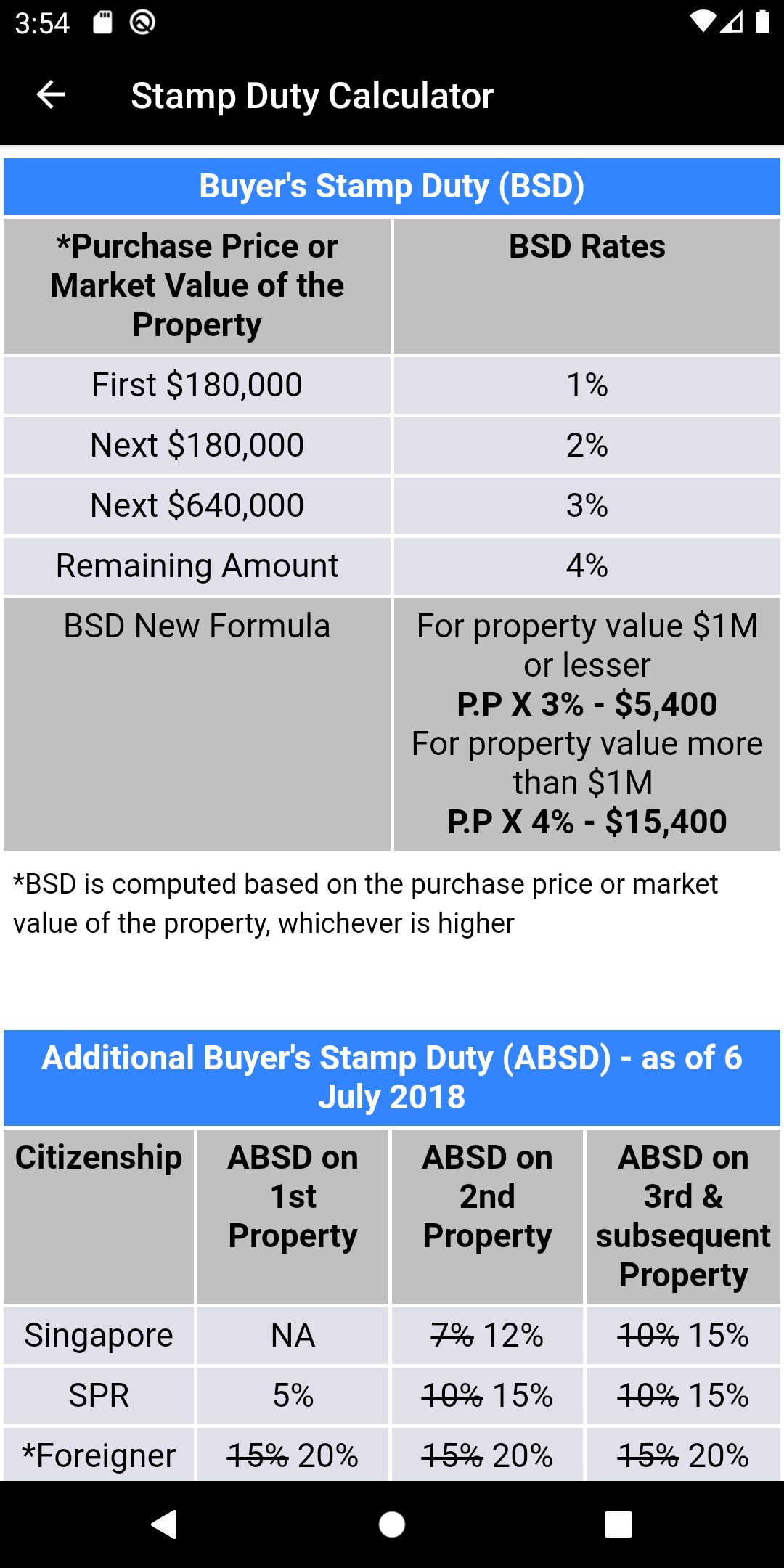

With the latest addition of 📃Stamp Duty Calculator, you can now start by understanding how Stamp Duties are being calculated, and then work out the amount payable on your next residential property purchase!

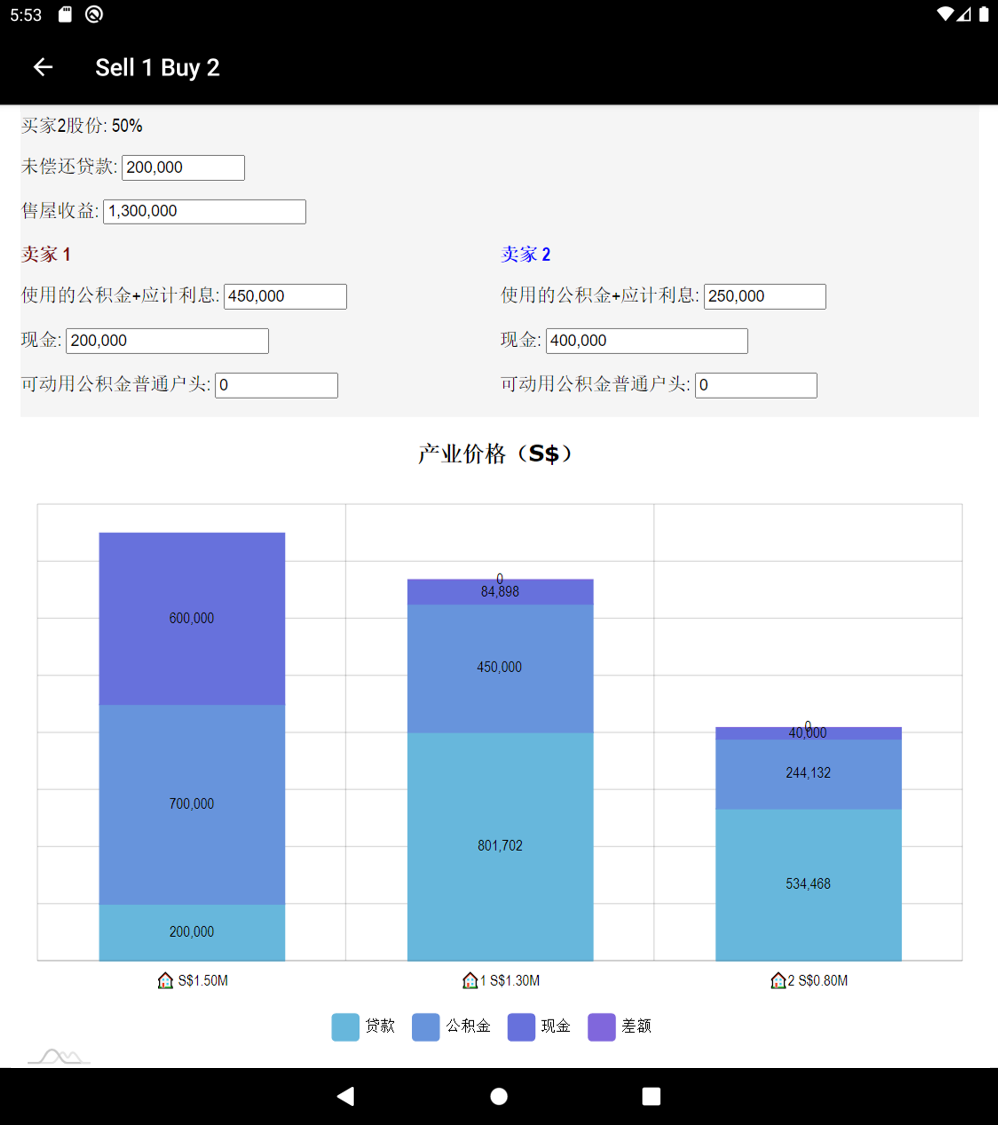

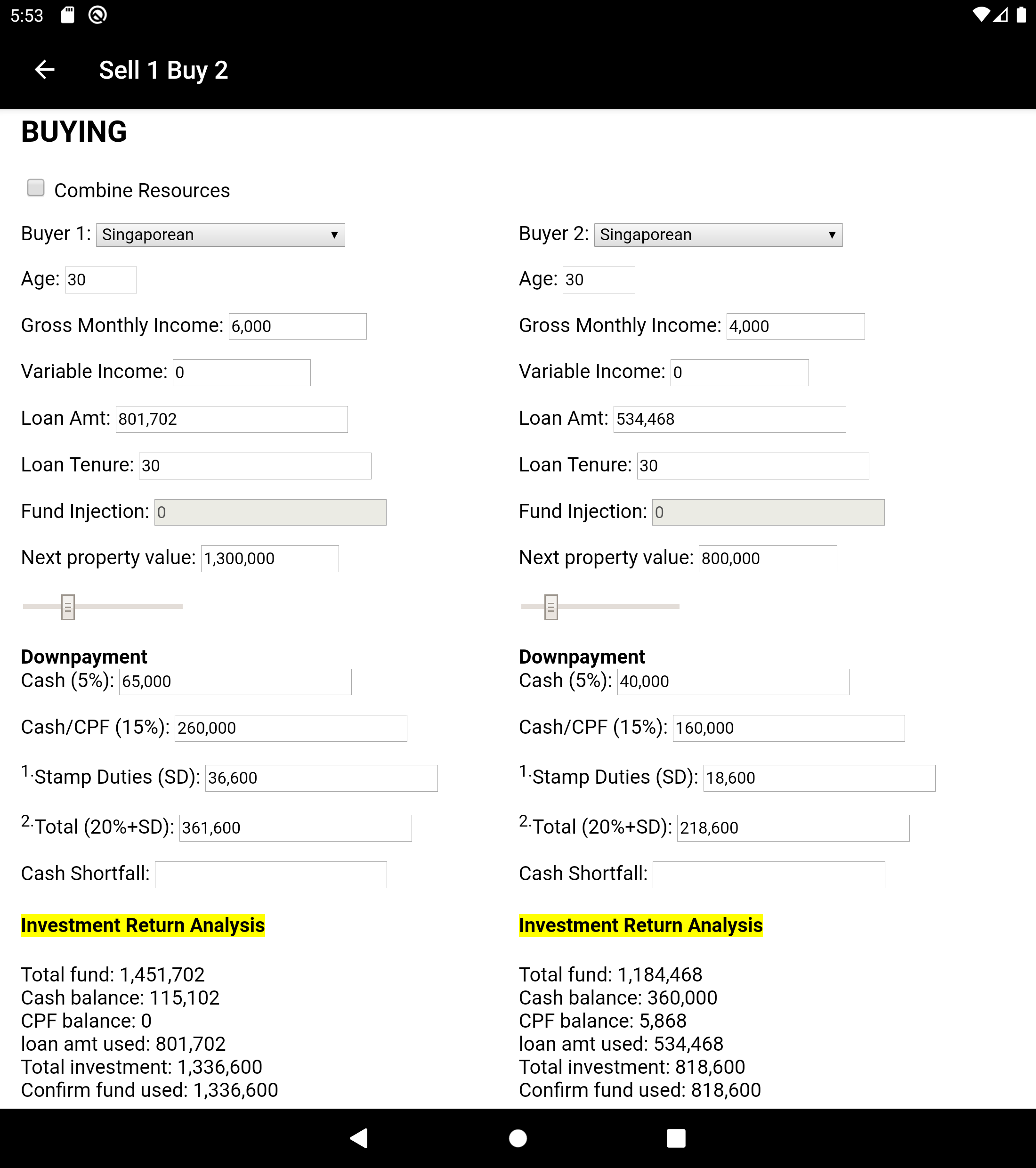

This calculator is meant to give you an idea on the various options to allocate your funds after selling your current property.

This strategy works well if you own only one property, and it is co-owned by your spouse, or was bought under tenancy-in-common.

Don't be misled by the title. It doesn't mean you have to literally "Sell one property and Buy another two".

Let's look at the options you could explore:

1) Sell your current property, buy one and then buy the next one sometime later.

2) Sell your current property, and just buy a replacement home.

The purpose of this move is to improve or preserve the value of your property with your available resources. One can change to a newer home so its value could possibly appreciate, or be sustained as the value of a property tends to depreciate as it gets older, which is especially true for HDBs.

On the other hand, it could also be an opportunity for home owners to savage the potential losses caused by a less-than-ideal property purchase.

For example, many HDB owners used up the entire CPF funds and savings to pay off the loan for their flats as soon as possible only to realise that when they wanted to right-size their flat to a smaller one, and cash out for retirement, they are unable to do so. Reason being, they are likely to end up with a negative sale as the capital gain (if any), have to be ploughed back into the accrued interests incurred over the years.

By restructuring your asset portfolio at an earlier stage, you could have a better chance of enjoying a capital gain out of your current property, redistribute your funds, and then leverage on the potential capital appreciation from the new property/properties.

此计算机旨让你了解出售现有房产后重组资金再做投资的可行选择。

这概念适用于夫妇同时拥有同一个房产,或者是买家以分权拥有的方式购买的房产。

不要被标题误导,这并不意味着您一定要”出售一个房产并购买另外两个房产“。

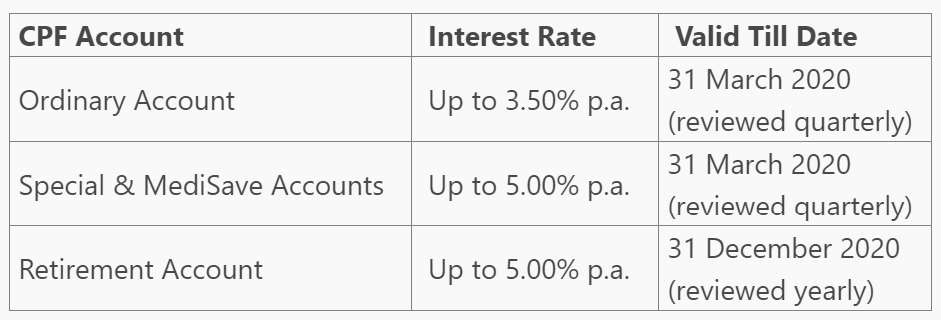

As you probably already know, the CPF prevailing interest rate is higher than the banks' current interest rate of below 2%. As an icing on the cake for borrowers, the Federal Reserve would be cutting interest rate near to zero in view of the current situation.

As you can see, it's a no brainer for one to leave more cash in CPF to earn the interests! 😎

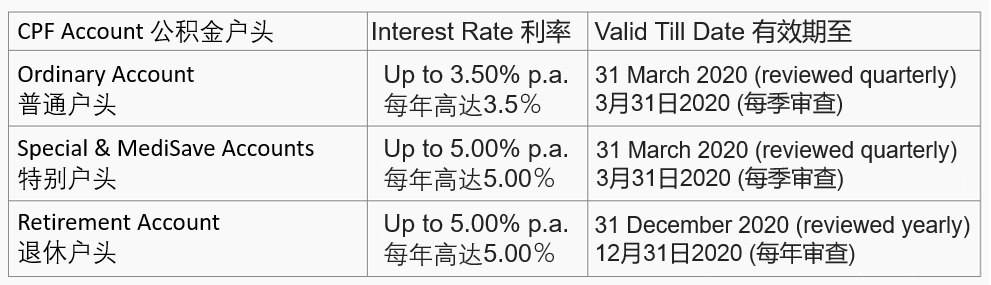

你可能已经知道,公积金利率是高于银行利率,目前银行利率甚至低于2%!基于目前的情况,美联储将降息至接近零。

正如您所看到的,将更多的现金留在CPF中以赚取利息更为明智之举! 😎

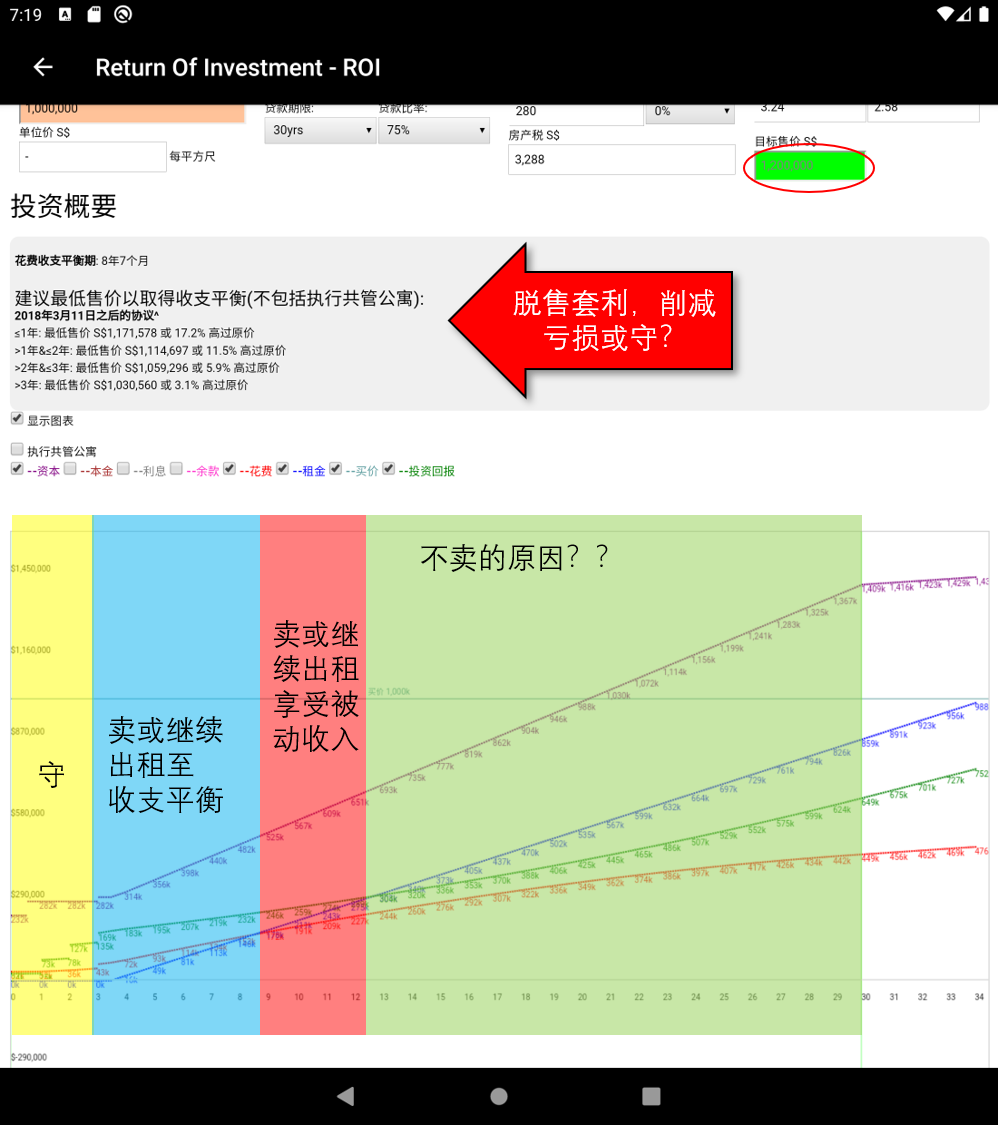

Investment Return - ROI or ROE投资回报

In a property purchase cycle, it is likely you will encounter one or more unfavourable downturns, the next best thing you can do is to understand the whole process, and identify the exit strategies.

With this ROI chart, you can better gauge the time to capitalise on your assets and if necessary, when to cut loss, etc.

在整个拥屋周期中,您可能会遇到一个或多个不利的低迷时期,唯一可以掌握的是了解整个置产过程,并拟定退场策略。

使用此投资回报率图表,你可以更好地策划持产时间表,并在必要时减少损失等等。。

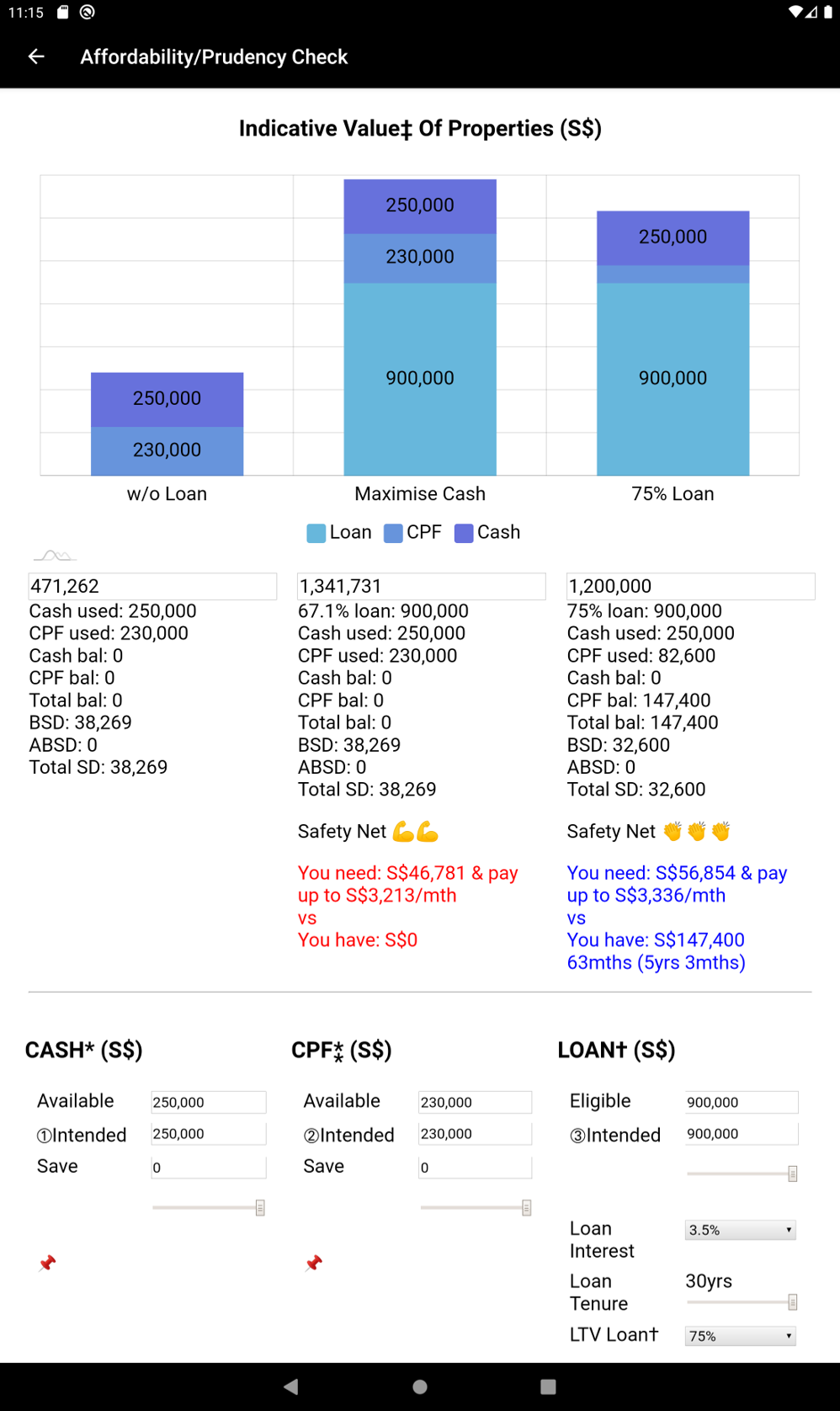

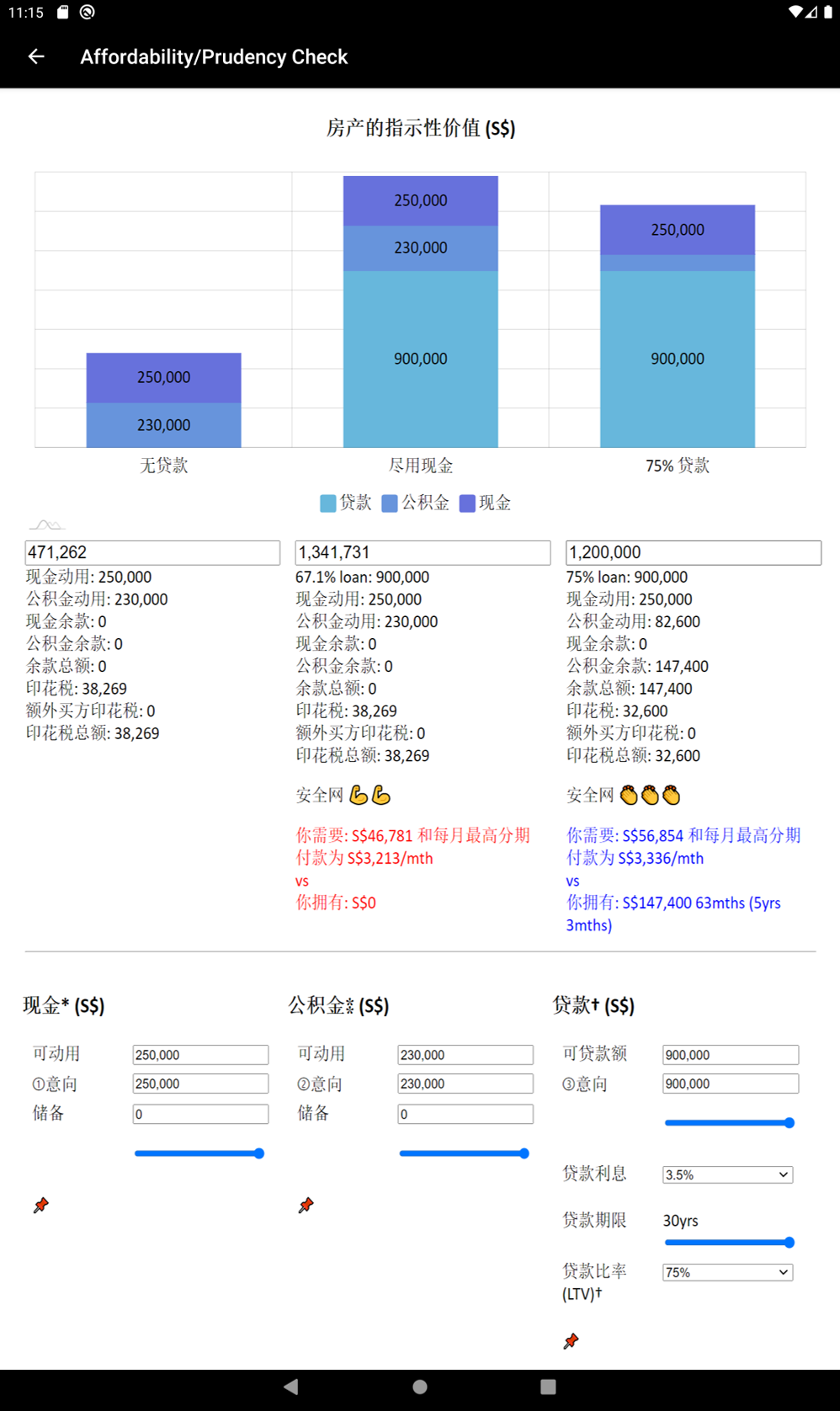

Affordability/Prudence Check负担能力/审慎性检查

To curb speculation which in turn drives up property prices, the government implemented its 1st round of cooling measures on 20 February 2010. A seller will need to pay a stamp duty (Seller Stamp Duty; "SSD") if the property is sold within a time period from the year of purchase. After 3 rounds of intensified adjustments to the SSD, the latest which was the 4th round of adjustment effective on 11 March 2017 provides a relexation of the levy. Currently, the law requires the seller to pay a stamp duty of 12%, 8% and 4% if the property is sold within 1, 2 and 3 years respectively from the date of purchase. This works out to a hefty sum of money and potential buyer will need to take this into consideration during a purchase.

为了遏制投机活动,进而推高房地产价格,政府于2010年2月20日实施了第一轮降温措施。如果在限制期内出售该房产,卖方将需要支付一笔印花税(卖方印花税;“ SSD”)。之间金管局又在对SSD进行了三轮强化调整之后,最后的一次则是2017年3月11日生效的第四轮调整,对征费进行了松绑。至目前为止,法律规定是如果在购买之后的1年,2年和3年内(之前是4年)出售房产,卖方应支付12%,8%和4%的印花税。这也是一笔不菲的数目,所以潜在买家在购买时需要考虑到这一点。

For more information on SSD, please refer to

有关SSD的更多信息,请参阅 IRAS

Safety Net安全网

Buyers are advised to set aside a reserved fund in order to hold on to the property in the event of unforseen circumstances or temporary loss of income. This is to ensure that one is able to continue servicing the mortgage loan till he is able to rent out the place or dispose off the property without losses. As a guide, to avoid the need to pay the SSD, the seller is advised to dispose off the property only after 3 years.

This illustrative calculation takes into consideration the progressive payment of a newly launched project at different entry points. The reserved funds (safety net) formulation is based on the amount of capital outlay for the next 3 years or to the point when the unit is rented out to offset fully or partially the monthly mortgage installments. The calculation assumes the worst scenario where there is no income during this 3yr period.

Basically, this reserved fund required ranges from about 5% to 15% of the property value depending on when purchase is made. Thus, to minimise the capital outlay, the best timing to buy a new property is during the initial launch phase.

这里建议买家预留储备金,以便在无法预料的情况下如短暂失业或出现周转困难时能继续偿还每月贷款,直到能出租或在无需缴付额外关税下出售房产为止。为避免支付SSD费用,建议卖方在3年后才脱售房产。

这计算法以不同进场点为起点(如新项目的逐步付款方式)来计算所需资金。预留资金(安全网)的公式是基于接下来3年所需的资本支出,或至得以出租该单位以完全或部分抵消每月贷款的期限为基础。该计算假设最坏的情况是在这三年期间零收入。

基本上,这笔储备金的要求范围为房产价值的5%至15%,取决于购买时间点。因此,为了最大程度的减少资本支出,最佳购买时间机是在新项目刚开盘的阶段。

How does this calculator work?这个计算机如何运作?

Simply key in the available source of funds into the repective funds input boxes. Adjust the values ➀, ➁ & ➂ and find out the indicative property prices with the best safety net coverage that you would like to have.

You need to have a basic knowledge of how CPF and Bank loan work. There are pointers along the way in the calculator. Just play around with the figures and you will be able to work out a proposition that will fulfill your investment requirements.

In case you need any clarification, please feel free to contact us at +65 9066 6966 or send us your Enquiry for a non-obligatory discussion. 🤠

只需在各资金来源格中输入可用资金即可,再调整➀, ➁ & ➂款额并找出您想要拥有的最理想的安全网覆盖率的指示性房产价格。

最佳为你能略懂公积金使用和银行贷款的审批条规。然而计算机里也会有旁注,只要反复实验性的调整数额,你就能设定出符合您投资要求的建议。

如果您需要任何澄清,请随时与我们联系+65 9066 6966或传发送给我们您的问题或疑问 🤠