The two main factors which determine your ability to own a private property (or HDB) are Eligibility

& Affordability.

Before you step into a show flat (or resale market), it is good to have a basic understanding of your

Buying/Holding Power and the Payment Process.

This guide will allow you to have an idea of the estimated value of the property that you could comfortably

afford.

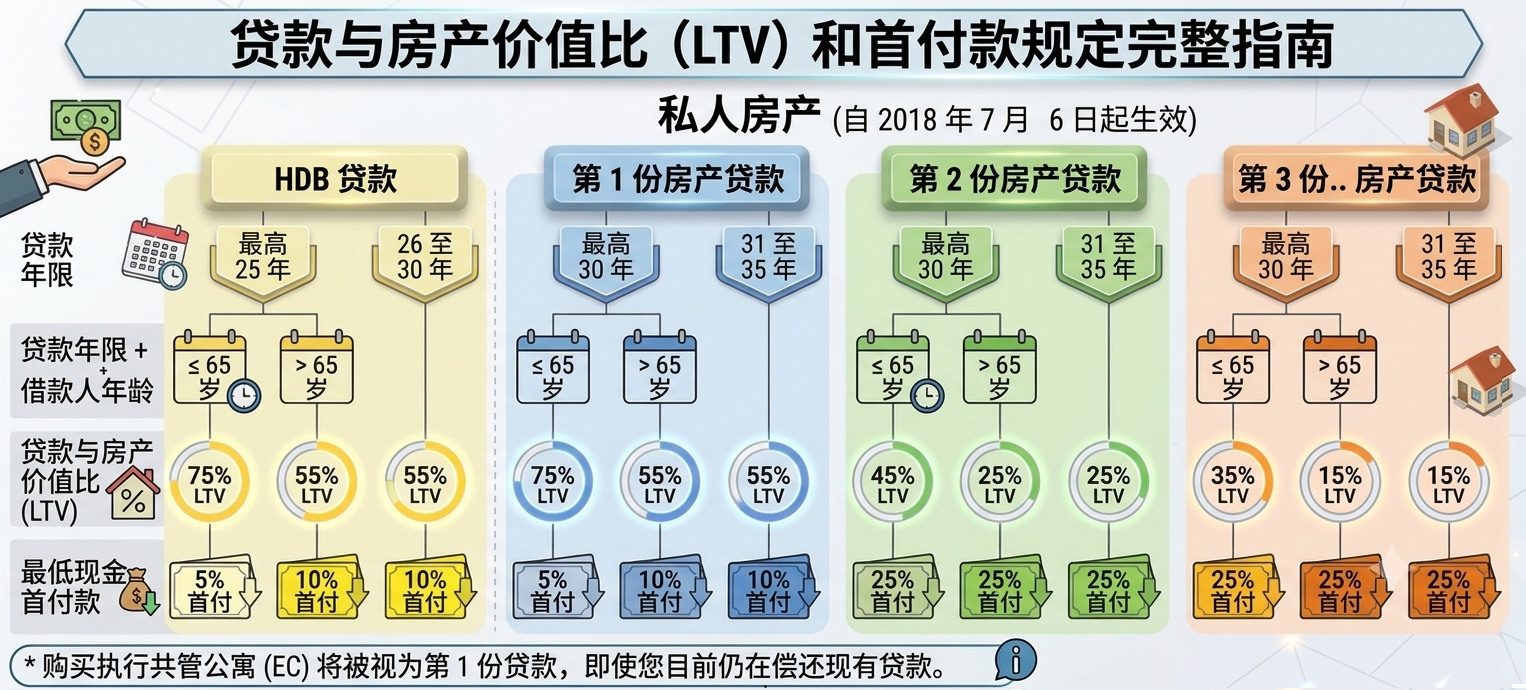

当你决定想拥有私人房产或政府组屋,两个主要考虑因素是政策符合和负担能力。

当你踏入展销厅(或转售市场)之前,最好先了解您的可负担能力和付款流程。

本银行借贷指南让你对可贷项款百分比有个概念。

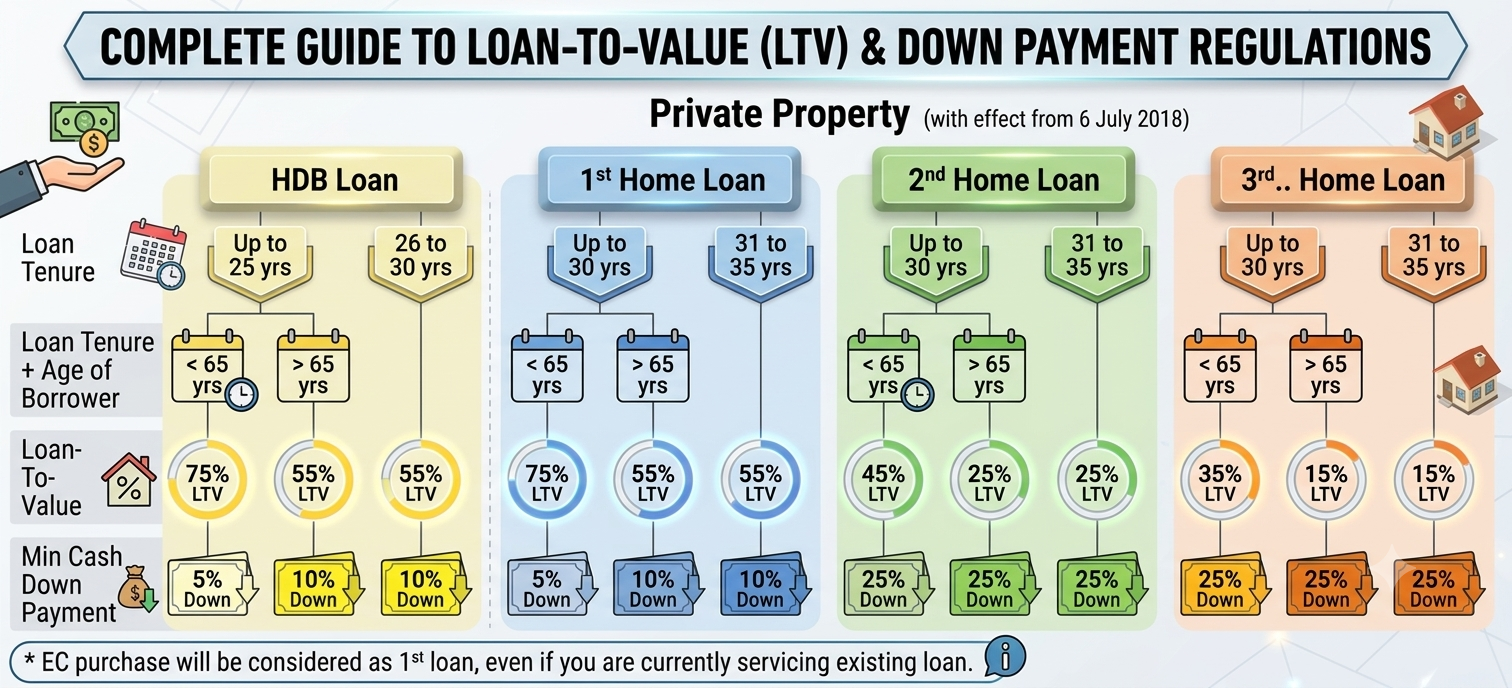

Firstly, you'll need to find out the percentage of 🏦Loan you could possibly borrow from a bank,

e.g. 50%, 60%, 75%, etc. This will determine how much Cash💵 and CPF💲 components you need

for the purchase.

首先,您需要知道能从银行🏦借贷款项的百分比,例如50%,60%,75%等。这将确定您需要预备多少

现金💵和公积金存款💲。

Firstly, you'll need to find out the percentage of 🏦Loan you could possibly borrow from a bank,

e.g. 50%, 60%, 75%, etc. This will determine how much Cash💵 and CPF💲 components you need

for the purchase.

首先,您需要知道能从银行🏦借贷款项的百分比,例如50%,60%,75%等。这将确定您需要预备多少

现金💵和公积金存款💲。

If you are buying a private property, you'll need to calculate your loan quantum based on TDSR (Total

Debt Servicing Ration) and, both TDSR and MSR (Mortgage Servicing Ratio) if you are buying an

Executive Condominium.

If you are buying a private property, you'll need to calculate your loan quantum based on TDSR (Total

Debt Servicing Ration) and, both TDSR and MSR (Mortgage Servicing Ratio) if you are buying an

Executive Condominium.